Let's talk about FIAs

Fixed Indexed Annuities for a safer retirement

- Protect principal

- Provide modest, market linked upside

- Offer predictable, contractually guaranteed income for life

Why FIAs matter

Strengths & Highlights

Principal protection

Your money doesn’t go backward due to market losses. For many retirees, avoiding sequence of returns risk is a huge deal.

Annual “lock in” of gains

Once interest is credited, it becomes part of the new protected base. This is one of the most attractive features for long term planning.

Lifetime income options

This is the “personal pension” angle. For people without a traditional pension, FIAs can create a predictable income floor.

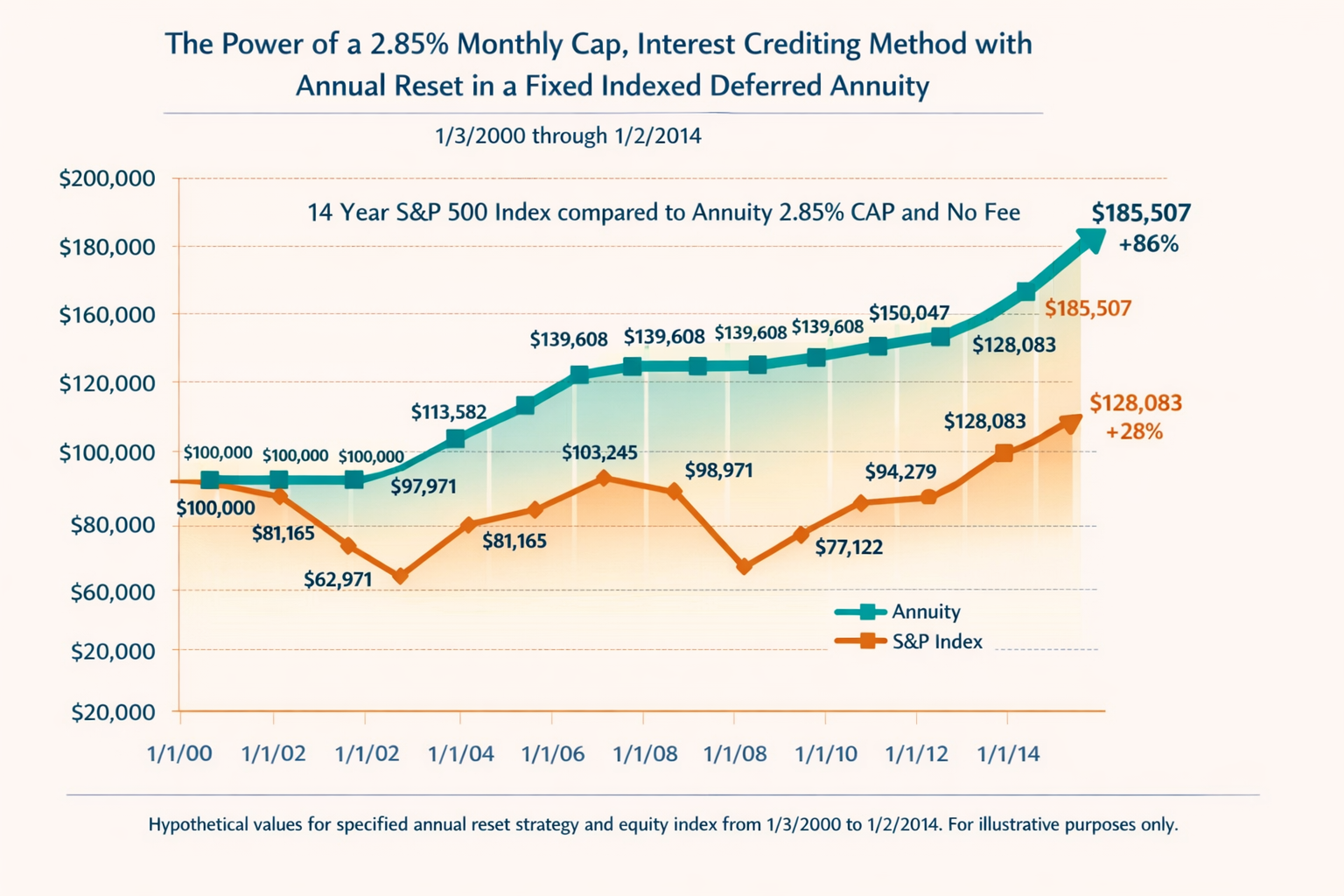

Market linked growth without market exposure

FIAs track an index but don’t invest in it. That’s how they can credit interest when markets rise but avoid losses when markets fall.

Behavioral benefit: no panic, no euphoria

FIAs remove the emotional roller coaster of market investing. That alone can be worth a lot for some people.

Understanding FIAs

A More Balanced View

1. Caps, spreads, and participation rates

These limit how much of the index’s upside you actually receive.

- A 5% cap means even if the index rises 20%, you might only get 5%.

- Some products use participation rates instead (e.g., 40% of the index gain).

These terms can change over time, depending on the contract.

2. Surrender periods

FIAs are long term vehicles - often 7 to 12 years. They’re not meant for liquidity

3. Income riders cost money

The “double your income base” feature usually comes from an optional rider with an annual fee. It’s valuable, but it’s not free.

4. Outperforming-the-market depends on the timeframe

FIAs outperform the market only in periods with large drawdowns. Over long bull markets, they typically lag because of caps and participation limits.

5. Insurance company strength matters

FIAs are only as strong as the issuing insurer. Legal Reserve Life Insurance Companies are heavily regulated, but it’s still smart to check ratings (AM Best, Moody’s, S&P).

So… Be Safe or Gamble?

FIAs make sense when:

- You want guaranteed income for life

- You want to protect principal

- You want predictable growth

- You want to cover essential expenses with something stable

- You dislike market volatility

FIAs make less sense when:

- You want high growth potential

- You need liquidity

- You’re comfortable with market risk

- You prefer managing your own investments

A Thought to Consider

- FIAs for essential expenses

- Stocks/bonds for growth and discretionary spending

- Cash for short term needs